Key Takeaways

1. SOC 2 automation involves implementing software tools and systems to streamline and automate processes to achieve compliance with SOC 2.

2. SOC 2 compliance automation can be prone to misuse and cybersecurity risks. Automation software can produce unnecessary information and gaps in compliance that are easy to miss due to over-reliance on the program.

3. IS Partners’ expert CPAs perform SOC 2 audits. Our team can also work if your service organization uses existing software.

What is SOC 2 Automation?

SOC 2 automation is the use of compliance software to streamline the compliance process for SOC 2 certification. This type of software is used to document the necessary evidence for a service organization to pass SOC 2 requirements.

Compliance automation of SOC 2 was developed to help make audits easier for auditors and service organizations. It captures real-time information for monitoring and eliminates the need for manual data collection.

What Can Be Automated for SOC 2?

SOC 2 compliance tools are meant to automate repeatable tasks that are critical for achieving and maintaining SOC 2 compliance.

Ideally, the key features of SOC 2 automation should include the following:

- Automatic documentation

- Continuous monitoring

- Policy development from templates

- Risk assessment and management

- Breach alerts and notifications

- Reporting

- Access controls

- Vendor management

Each compliance automation software will vary depending on its complexity. SOC 2 automation is meant to help auditors and not to replace their expertise and certified judgment.

Test Your SOC 2 Readiness Today

Start a free self-assessment quiz and get a customized report.

What Can’t Be Automated for SOC 2?

Despite the many features and advantages of SOC 2 automation, it still has limitations. One of which is their reliance on human judgment and information feeding.

Because of these and other factors, the following aspects of SOC 2 compliance cannot be automated:

- Informed decision-making

- Security control design

- Incident response and

- Auditor communication

- HR-related tasks

- Adaptation to business continuity

SOC 2 compliance automation tools still require human intervention. The information that it generates must also be validated to avoid any errors that might occur from inconsistent input.

Advantages of SOC 2 Compliance Automation

Utilizing software to automate the SOC 2 audit process offers several advantages for both service organizations and auditors. SOC 2 compliance automation can help finish tedious and repetitive compliance tasks faster than human employees.

Looking into the advantages of automation, here are some:

Enhanced efficiency

SOC 2 tools can improve the efficiency of service organizations through documentation and automated evidence collection and organization in a central repository or integrated data connections. This allows service auditors easier access to the information and for audit preparation.

Faster Gap Analysis

Some automated SOC 2 compliance tools can quickly identify gaps in your system. This tool can determine which parts of the SOC 2 framework you have already fulfilled and which parts require more attention.

Improved Management

Some automated SOC 2 tools may enable service organization management to perform functions—like risk assessment, vendor management, and control monitoring–more effectively.

Streamlined Audit Process

Automation facilitates audit readiness by maintaining up-to-date documentation, evidence of compliance, and audit trails. Automated tools can generate comprehensive reports and documentation required for SOC 2 audits, simplifying the audit process and reducing the burden on internal teams.

Easier Compliance Maintenance

Compliance tools are also meant to help maintain compliance. Tools help you to document deviations and monitor your compliance consistency throughout operations. The information the software gathers can help you identify which areas to focus on for the next SOC 2 audit for continuous compliance.

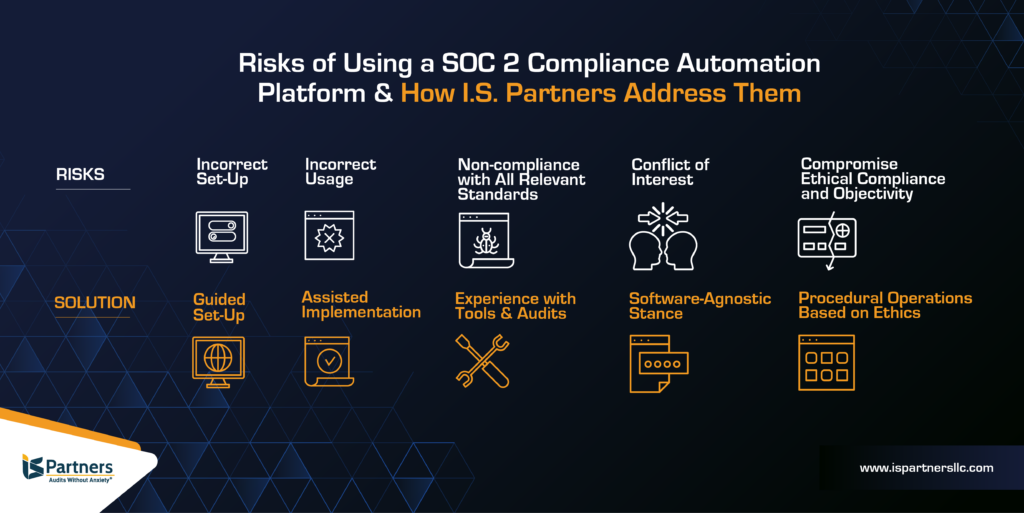

SOC 2 Automation Risks When Using Compliance Software & How IS Partners Experts Address Them

Although using software to automate the SOC 2 audit process can offer many benefits, there are also potential risks associated with its implementation. Some of these risks include incorrect set-up or configuration of the tool, which could lead to inaccurate information and improper conclusions in the audit.

It is essential to properly manage these risks to ensure a successful and accurate SOC 2 audit process. In this section, we listed some of the critical risks of a SOC 2 compliance automation platform and gathered solutions from IS Partners’ compliance experts.

Risk: Incorrect Set-Up

Tools must be properly designed, configured, and managed to provide the expected benefits. If the SOC 2 software is not set up properly, it may give the service auditor wrong information, leading to incorrect conclusions in the SOC 2 examination. For example, if the tool doesn’t collect data correctly from your organization’s systems, it may show inaccurate information.

Solution: Guided Set-Up

No tool is perfect; they all have their challenges, and we are good at identifying what those are and how to work around them. A lot of these tools will automatically generate a set of custom controls and a set of requests in preparation for a SOC 2 audit.

Yet, every client’s environment is different, and every audit looks different in real life. We help our clients from the very beginning to make sure that everything is set up correctly.

Risk: Incorrect Usage

Suppose your organization’s management lacks the skills or knowledge to automate SOC 2 properly. In that case, they might heavily rely on the tool’s built-in features, such as its risk assessment function, list of common controls, or library of policies and procedures.

As a result, management may not be able to take responsibility for designing and maintaining effective controls to meet their commitments and system requirements.

Solution: Assisted Implementation

IS Partners is agile; we’re proficient with technology and adept at understanding and utilizing software tools to deliver an end report successfully. As a firm, we understand fully the details of the Trust Services Criteria.

We have a reasonable grasp of the points of focus within the SOC 2 framework, so we understand how to enable software tools to accurately reflect our clients’ control environments and enable the request process to ensure that we are getting adequate evidence for the audit.

Risk: Non-compliance with All Relevant Standards

Service auditors must ensure that using a SOC 2 tool does not change their responsibilities to comply with relevant professional and ethical standards. SOC 2 automation tools may try to fit a service organization’s security control into a single, general model. This can create gaps across other relevant frameworks or amendments in the SOC 2 audit process.

Solution: Experience with Tools & Audits

IS Partners’ auditors really know the points that need to be addressed for a comprehensive SOC 2 audit. A tool, on the other hand, may not address all those points in the TSC.

We’ve seen instances where some documentation is missing or the tool is not guiding the client along industry best practices. So, we work with our clients to resolve those challenges. Our end goal is to make our clients’ lives easier.

Risk: Conflict of Interest

Certain business relationships between service auditors and SOC 2 tool providers may threaten the auditor’s compliance with professional and ethical responsibilities. There could be circumstances where using an automated SOC 2 platform can threaten the service auditor’s independence, especially if the tool provider is considered a subservice organization that’s part of the examination.

Solution: Software-Agnostic Stance

We will always maintain our independence as a firm and examine what we see accordingly. We talk frankly with our clients and ask questions about every control to make sure that we maintain our objectivity in the entire process—regardless of the software platform they are using.

Risk: Compromised Ethical Compliance and Objectivity

Depending on the relationship between the service auditor and the software provider, some situations may threaten compliance with ethical rules and professional objectivity. For example, if the software provider promotes the service auditor’s services and offers discounts on the auditor’s fees or if the auditor pays the SOC 2 software provider for client referrals.

Solution: Procedural Operations Based on Ethics

IS Partners doesn’t have exclusive relationships with any software companies. In fact, we maintain a software-agnostic stance in support of our ethical obligations and due diligence. We are serious about going into every engagement with an open mind and no expectations.

In any instance, whether we are using a software tool or starting from scratch, our clients could give us a set of controls and requests, but we re-validate all of that information. That’s built into our procedural operations when doing audits.

We perform re-validation of every control within an engagement specifically to maintain objectivity.

How Does Using a SOC 2 Compliance Tool Affect the Auditor’s Responsibilities?

The service auditor is in charge of conducting a SOC 2 examination according to the required guidelines. Although using a SOC 2 tool doesn’t change the auditor’s responsibilities, it might affect how the auditor carries out those responsibilities.

Here are a few examples:

- If management uses a SOC 2 tool’s list of common controls without customizing them to the organization’s specific needs, they might not address unique risks. For instance, a tool might suggest quarterly vulnerability scans, but an organization in a high-risk industry might require more frequent scans. Management must customize controls for the organization to prevent gaps in control design and impact the auditor’s opinion negatively.

- When management uses a SOC 2 tool to collect documents for the auditor, the software-generated information is considered information provided by the entity (IPE). Management is expected to verify the accuracy and completeness of this information. The auditor’s responsibility to obtain enough evidence to support their opinion remains the same. The auditor needs to verify the reliability of the IPE and may perform procedures to ensure the platform works as expected.

- If an organization uses an automated SOC 2 tool and services provided by the same company, the auditor needs to understand the processes and controls performed by the software. Management is responsible for determining if the software provider is a sub-service organization and addressing any risks and controls associated with them. If the software company is a responsible party in the examination, the service auditor must maintain independence from the software company.

This is why the AICPA advises that using a SOC 2 tool may affect how service auditors meet their responsibilities, but their primary responsibilities remain the same.

Can Using an Automated SOC 2 Compliance Tool Threaten an Auditor’s Independence?

Yes, there are circumstances where using an automated SOC 2 platform can threaten the service auditor’s independence.

If the tool provider is considered a sub-service organization and the service organization’s management chooses to use the inclusive method to describe the services provided by the subservice organization, the sub-service organization’s management would also be considered a responsible party in the SOC 2 examination.

In these situations, the service auditor must maintain independence from the sub-service organization.

Ethical Implications of Auditor’s Business Relationships with SOC 2 Automation on Objectivity and Compliance

Depending on the relationship between the service auditor and the software provider, some situations may threaten compliance with ethical rules and professional objectivity.

Discounts and Objectivity

For example, suppose the software provider promotes the service auditor’s SOC 2 services and promises clients a discount on the auditor’s fees. In that case, the auditor should refer to the “Integrity and Objectivity Rule” and the “Advertising and Other Forms of Solicitation Rule.” The auditor needs to ensure the software company’s offer is not false, misleading, or deceptive.

Referral Fees and Disclosure

If, for example, the auditor pays the SOC 2 software provider for client referrals, then the “Commissions and Referral Fees Rule” applies. The auditor should disclose the referral fee in writing to all new clients.

Audit Evidence and Reliable Accuracy

If the service auditor relies only on the SOC 2 tool to automatically collect evidence and wants to sign the SOC 2 report, they must still comply with the “Compliance with Standards Rule.” The auditor’s responsibilities in a SOC 2 audit don’t change because the service organization uses a SOC 2 tool and must ensure they follow all applicable standards.

Overall, the relationship between the service auditor and the SOC 2 software company matters, and the auditor should always ensure that they comply with the relevant ethical rules and professional standards.

While SOC 2 tools can offer efficiency and improved management for service organizations, they can also present challenges in maintaining security compliance status with professional standards and ethical rules for service auditors.

Auditors must be mindful of their responsibilities and potential conflicts of interest while using these tools. Ultimately, the key to successfully using SOC 2 tools is understanding their potential effects and diligently adhering to the professional and ethical guidelines established to maintain utmost integrity throughout the auditing process.

Work with Accredited CPAs with the Software of Your Choice

SOC 2 tools are not a replacement for a trustworthy CPA SOC auditor.

Unlike software-only solutions, IS Partners ensures that clients have the guidance needed to prepare for a SOC 2 audit and are ready to perform the actual audit. None of the testing is outsourced, and there is no need to engage another firm.

IS Partners is ready for this next step in SOC 2 audit automation. Our firm has decided to be software-agnostic, meaning that we are happy to work with clients on the software of their choice.

Clients can use our compliance management software, FieldGuide, or bring their own software. Either way, they get the efficiency and clarity that comes with using a SOC 2 tool, plus the expert advice of certified CPAs—at every step.

IS Partners has dedicated over 20 years to ensuring cybersecurity for service organizations. Our experts personally work in validating security controls, assessing risks and vulnerabilities, and implementing cybersecurity frameworks with no outsourcing involved.

Rely on IS Partners for dependable SOC 2 audits with or without the help of compliance software. Contact us today or set up a meeting with our SOC 2 experts.