Key Takeaways

1. Sarbanes-Oxley (SOX) Act is a federal law that meets financial reporting, information security, and auditing requirements.

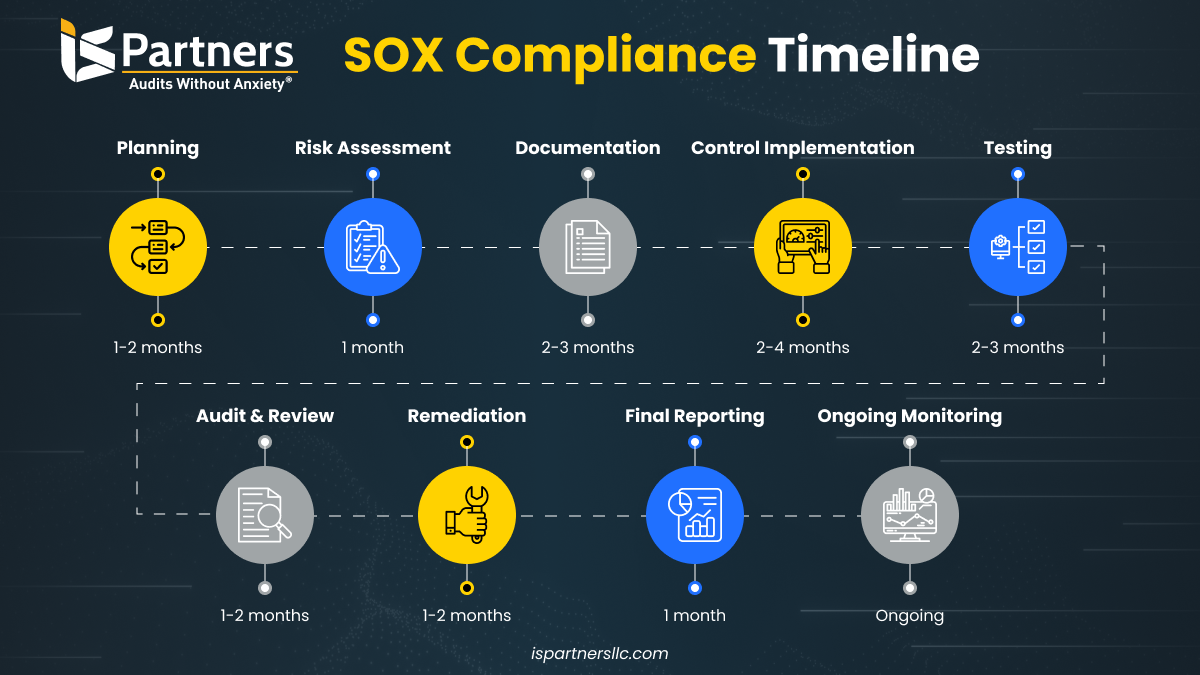

2. Achieving SOX compliance involves structured steps such as risk assessment, control implementation, and ongoing monitoring.

3. I.S. Partners can help you streamline your SOX compliance journey, aligning with legal standards and enhancing internal controls.

Steps to Implement SOX Framework for Compliance

Implementing SOX compliance involves establishing a comprehensive framework of internal controls and maintaining rigorous oversight to safeguard financial reporting accuracy.

The key steps for internal auditors to implement SOX compliance involve risk assessment, materiality analysis, evaluating SOX controls, and more. Let’s take a look at all the key steps in detail below:

Step 1: Plan the Timing of Your Annual SOX Audit

SOX compliance testing is an ongoing process conducted on a rolling cycle, with testing performed quarterly for interim and year-end (YE) roll-forward assessments. Rather than treating it as a one-time audit, organizations should integrate SOX testing into their internal controls framework throughout the year.

To align with reporting requirements, coordinate with your independent auditor to ensure the timely completion of testing before your annual report. Additionally, maintain a clear distinction between SOX compliance testing and other internal audits to prevent conflicts of interest.

Step 2: Risk Assessment

SOX risk assessment is the cornerstone of ensuring financial reporting integrity and maintaining a compliant control environment. It helps identify vulnerabilities in your information systems and ensures that the accuracy of financial statements is handled securely and accurately, shielding it from internal errors and security incidents.

However, if the assessment isn’t done right, it can lead to unnecessary headaches. Your team, management, and auditors could end up drowning in extra work, wasting time and resources. Worse, you might be left with controls that are either insufficient or improperly designed, leaving your organization exposed to material misstatements that could go undetected.

Now, let’s review how to perform SOX risk assessment in detail:

- Focus on Identifying Materiality. Start by pinpointing the financial metrics that truly influence decision-making. Materiality often ties back to percentages of assets, income, or revenue. Collaborating with executives can help establish meaningful benchmarks and highlight metrics with significant business or regulatory impact.

- Narrow your Scope. Determine which departments and locations warrant attention based on their materiality. Concentrate on areas like regional offices that contribute heavily to revenue while skipping smaller locations with minimal influence. This ensures your efforts are targeted and impactful.

- Following the Transactions. Understand how financial transactions move through your organization. The goal is to confirm that the published company’s financial statements accurately reflect real business activities. Work with process owners to validate metrics and uncover any gaps.

- Weigh the Risks (Quantitative and Qualitative). Evaluate risks on two fronts. Quantitative analysis tackles measurable issues like fraud or human errors, ranking them by severity to guide mitigation priorities.

- Identify IT Assets. Identify IT assets that play a role in financial reporting, from public accounting firms to accounting software and cloud storage systems. Ensure all relevant systems, including servers and databases, have the necessary control objectives to protect data integrity and compliance.

- Secure the System. Document and implement the controls that uphold financial accuracy. These include:

- Segregating duties to minimize fraud risks.

- Access controls and encryption to safeguard data.

- Reconciliation tools for error-free audit reports.

- Physical protections for critical assets.

- Monitor systems to evaluate and improve control effectiveness.

Step 3: Materiality Analysis

Materiality is at the heart of Sarbanes-Oxley compliance, which guides auditors in evaluating the weight and relevance of financial information. It is not to say just crunching numbers, but it involves determining which details are significant enough to influence decisions made by those relying on financial statements.

Materiality sets the bar for what could potentially sway a stakeholder’s perspective.

A material weakness becomes more important based on the extent of its potential impact. For example, if there’s a flaw in how revenue is recognized, it might lead to inflated or understated figures. Such discrepancies could seriously distort the company’s financial health as perceived by investors and regulators.

Here’s how to conduct a materiality analysis:

- Understand Materiality Thresholds. Define the financial thresholds that could influence stakeholder decisions, often based on a percentage of assets, revenue, or income.

- Identify Material Items. Pinpoint accounts, transactions, or metrics critical to accurate financial reporting.

- Engage Stakeholders. Collaborate with executives and auditors to align on what constitutes materiality for your organization.

- Evaluate Qualitative Factors. Consider non-quantitative elements like fraud risk, regulatory scrutiny, or reputational impact.

- Document the Criteria. Clearly record how materiality thresholds and items were determined for consistency in future assessments.

- Prioritize Risks. Focus controls and mitigation efforts on areas with the highest material impact.

Step 4: Identification of Key SOX Controls

As mandated by the Sarbanes-Oxley Act, SOX controls are designed to address and mitigate risks that could compromise the integrity of financial data. However, not every control within publicly traded companies falls under SOX jurisdiction, so identifying the relevant ones is critical.

To determine whether a control is applicable under SOX, consider the following:

- Does this control directly influence the financial data included in public disclosures?

- Is the control linked to any material financial accounts or the integrity of the financial statements?

- Does this control affect any systems, processes, or data streams that contribute to preparing financial reports?

If any of these apply, the control is likely relevant for SOX compliance.

Now, the most common SOX controls are:

- Access Controls. Limiting access to sensitive financial systems to authorized personnel only.

- Segregation of Duties. Ensuring no single individual has control over all aspects of a financial transaction.

- Change Management. Governing updates or changes to financial systems and processes to avoid unintended risks.

- Business Process Controls. Addressing operational risks within critical financial workflows.

- Data Backup Protocols. Safeguarding financial data against loss or corruption.

- Corporate Governance Controls. Reinforcing accountability and oversight at the management and board levels.

Step 5: Process and SOX Control Documentation

Properly recording each step of the process lays the groundwork for smoother management sign-offs on internal controls over financial reporting (“ICFR”) and gives auditors a clear picture to evaluate.

Keep detailed records of the review process, as they serve two critical purposes: addressing any questions auditors may raise and providing a strong foundation when the process is revisited in subsequent years. Engaging SOX specialists like I.S. Partners can smoothen this as our expert auditors offer practical strategies for efficient documentation and facilitation.

Step 6: Testing of Key Controls

SOX testing ensures a company’s internal controls over financial reporting are effective. This is a mandatory requirement for compliance. The testing process is typically divided into four key stages, each vital in verifying control integrity.

1. Initial Assessment

The process begins with walkthroughs to understand how controls operate. These walkthroughs are documented, often using flowcharts or narratives, alongside evidence showing the implementation of control activities.

What happens during this assessment?

- Controls are assessed for design adequacy and operational effectiveness.

- Any gaps identified are addressed through corrective action plans to avoid security breaches or cyberattacks.

2. Interim Testing

Midway through the year, the SOX program team revisits controls to ensure earlier issues have been resolved and the controls remain effective.

What happens during this stage of the SOX control testing?

This stage focuses on testing the effectiveness of existing controls. It does not evaluate whether processes have changed but ensures that controls continue to function as designed. Any process changes identified separately may require adjustments to controls and documentation outside of the testing process.

3. Year-End Testing

Toward the year’s end, the audit team conducts a final round of internal testing.

What happens during this stage of the testing?

- Controls with previous deficiencies will undergo retesting to verify that remediation measures were successful.

- The focus here is on operational effectiveness and ensuring all issues have been addressed.

4. Independent Auditor Testing

External auditors conduct the final phase of SOX regulations testing.

What happens during this stage of the testing?

- This third-party evaluation ensures an objective review of control effectiveness.

- The SOX team and management quickly address any findings from external testing, clearly documenting mitigating steps and process updates.

Step 7: SOX Deficiency Assessment

This step involves examining any gaps or weaknesses in the controls and determining their impact on financial reporting.

When assessing deficiencies, accountants need to:

- Identify specific areas where controls are failing or insufficient

- Understand the root cause of these gaps, whether it’s a process issue, a lack of resources, or outdated protocols

- Prioritize deficiencies based on their potential impact on financial reporting and compliance

In the end, timely action is critical. Hence, you need to address these weaknesses promptly to strengthen the control environment and ensure the integrity and reliability of financial statements. Here’s how you can do this:

- Gather Evidence. Collect documentation and reports from internal audits and control tests to identify where deficiencies exist.

- Analyze Control Gaps. Evaluate the root cause of each gap by considering factors like process design flaws, operational efficiency errors, or resource limitations.

- Assess Severity. Determine whether the deficiency is significant or material by assessing its potential impact on financial reporting and compliance.

- Develop a Remediation Plan. Create a step-by-step plan to address the identified issues, including assigning responsibilities and setting timelines.

- Implement Corrective Actions. Put the remediation plan into action, focusing on strengthening controls and improving processes.

- Retest and Validate. Once corrective actions are implemented, retest the controls to ensure effectiveness and reliability.

Step 8: SOX Reporting

The final phase of SOX compliance is preparing the SOX control report, which is a critical document that summarizes the results of compliance testing. It outlines the organization’s control environment.

It also highlights how well internal controls function to prevent fraud and errors, serving as a testament to a company’s commitment to integrity.

What does the report include?

- Control Assessment. A thorough evaluation of the effectiveness of internal controls across key business processes that shows your organization’s compliance through and through.

- Control Deficiencies. This section should detail any weaknesses found during testing. Based on their impact and severity, they can be categorized as significant deficiencies or material weaknesses.

- Remediation Plans. Have an actionable roadmap that addresses any identified deficiencies. It should specify steps and timelines for improvement.

SOX Compliance Requirements

There are certain SOX compliance requirements you must adhere to implement, and they are:

- Submitting Audited Financial Reports to the SEC. Accurate, audited financial statements must be provided to the Securities and Exchange Commission (SEC) to ensure transparency and accountability.

- Establishing a Formal Data Security Policy. A robust data security policy must be created and enforced to protect sensitive information and maintain the integrity of financial data.

- Disclosing Significant Changes in Real-Time. Any major developments impacting financial performance must promptly disclose to the public, ensuring stakeholders are informed.

- Developing and Testing Effective Internal Controls. Design, implement, and regularly test internal controls to mitigate potential risks and verify the reliability of financial reporting.

Who is Allowed to Conduct SOX Audits?

Only independent external audit firms are authorized to conduct SOX audits. This separation is a key requirement under the Sarbanes-Oxley Act to ensure auditors remain impartial and free from conflicts of interest.

That’s where I.S. Partners steps in. With our specialized expertise, we help strengthen your overall SOX strategy, ensuring SOX compliance with accurate financial reporting and solid internal controls. Plus, we enhance your business value through improved security and control practices.

Compliance with SOX 404 requires that companies implement an internal audit function to perform quarterly testing of key controls. Full-scale implementation of control testing for key controls is a key component of the services I.S. Partners provides

Our team supports organizations in meeting SOX 404 requirements, providing expert guidance, streamlined compliance processes, and tailored audit solutions. Contact us today to ensure your business stays compliant and audit-ready.

SOX Best Practices

Implementing SOX compliance requires you to follow some best practices to be prepared for the audit with no surprises during the external audit. Let’s explore key strategies to smoothen your approach to SOX compliance.

1. Build a Robust Monitoring Framework. The first best practice you must implement is building a well-designed continuous monitoring setup. This ensures that critical processes and metrics are always under the microscope.

2. Tackle IT Systems and Manual Controls. Manual controls often step in to verify data integrity through reconciliations and adjustments. Each time a control is executed, ensure the sensitive data’s accuracy and completeness are reviewed.

4. Keep Unauthorized Changes in Check. Track changes diligently and flag discrepancies. If you alter one control, assess how that tweak impacts the rest of your program to avoid ripple effects.

5. Leverage Control Matrices. A control matrix maps out the identified risks, processes, and activities tied to your business operations and pairs them with your implemented control security measures. This proactive approach makes it easier to manage internal controls and spot gaps before they become problems.

7. Conduct Regular Internal Audits. Internal audits help uncover weaknesses in your financial reporting processes, allowing your team to implement controls. Make sure to conduct it regularly.

8. Consider External Auditors. Given the complexities involved, outsourcing audits to external auditors is a wise choice. Their independent, unbiased perspective validates your regulatory compliance efforts and identifies areas you might have overlooked.

Achieve Seamless SOX Compliance with IS Partners

Implementing SOX compliance is a complex yet essential process that ensures financial reporting integrity, protects sensitive data, and meets regulatory requirements. The key to success lies in structured risk assessment, robust internal controls, and continuous monitoring.

At IS Partners, we specialize in guiding businesses through SOX compliance with expert-driven strategies, tailored audit solutions, and seamless integration of control testing. Our team ensures that your organization meets SOX 404 requirements while minimizing risks and streamlining reporting processes.

What Should You Do Next?

Follow these steps to streamline SOX compliance for your service organization.

Conduct a Comprehensive Risk Assessment. Identify material financial risks, evaluate IT controls, and establish security measures to protect data integrity.

Implement and Test Key Controls. Develop a strong control framework, conduct regular testing, and address deficiencies before external audits.

Engage with IS Partners. Our compliance experts will help you navigate SOX requirements with efficiency and confidence, ensuring audit readiness and regulatory success.

Stay ahead of compliance challenges. Schedule a call with our experts today and take the next step toward a secure and compliant financial environment.